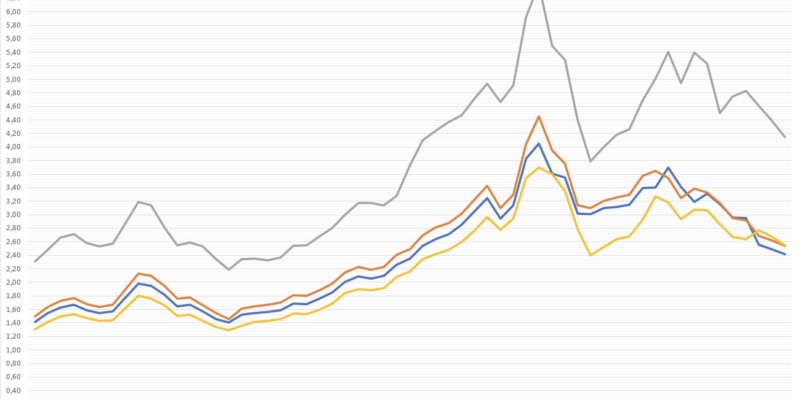

While the third quarter saw a downward trend in steel prices, it seems that the low point has been reached.

The fourth quarter saw a slight upturn in prices. In Europe, this was mainly the result of production cutbacks at major producers such as Arcelor Mittal and Tata Steel, which shut down several blast furnaces for maintenance and inspection. This reduction in production volumes is also evident at global level, with output down by 5% in China.

This limitation of volumes has had its effect. In Europe, this was coupled with specific measures in certain countries, such as Germany, to boost the competitiveness of their industry and thus maintain prices.

There has also been an increase of around 8% in motor vehicle production, particularly in Germany and China, which has supported price rises.

In the stainless steel market, the downward trend in alloy surcharges continued. However, stainless steel prices remained relatively stable over the period because the rise in steel prices offset the fall in alloy surcharges.

For the beginning of 2024, depending on the commodity, the price of a tonne of steel will vary between €740 and €890 per tonne.