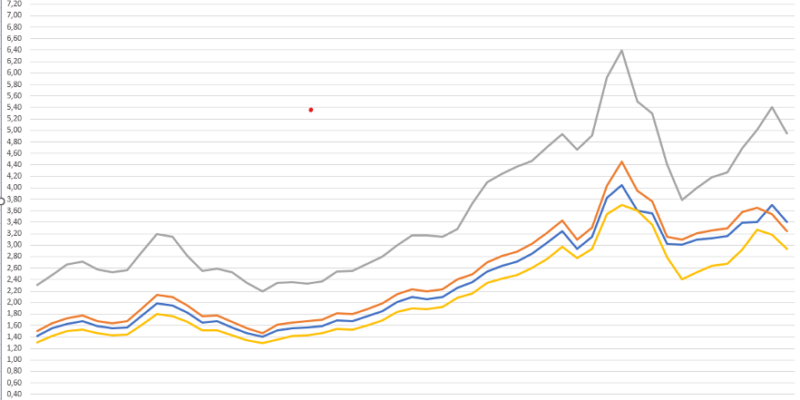

Steel prices were more or less stable in Europe in the first quarter.

However, due to certain incidents at the level of certain producers (blast furnace fire at Arcelor Mittal and planned maintenance at Tata Steel), there is a risk of a decrease in available tonnages. Arcelor has announced a reduction of 1 million tonnes.

This has already led to some increase in delivery times, but it cannot be excluded that supply will fall short of demand, which will have an effect on prices. We are already seeing a slight upward trend of between €50 and €100 per tonne in April compared to March. We must not forget to add to this the energy surcharges which vary from producer to producer between €100 and €200 per tonne.

Chinese production is currently almost entirely absorbed by the domestic market and Chinese companies will do everything in their power not to let prices fall. The same is true in Turkey, where domestic demand is strong after the earthquake and reconstruction needs.

As far as alloy surcharges for the various stainless steel grades are concerned, prices are also relatively stable. There was a slight upward push in February and March but in April prices are back to the level of January prices. These elements coupled with the evolution of steel prices do not currently indicate a likelihood of a strong increase in the short term.